Mortgage calculators are a great way to figure out if you can afford a home, but depending on which one you use, some may be more accurate than others.

Most calculators, like those from real estate giants Zillow and Redfin, show you a pretty decent estimate of your potential monthly payments, but they don’t exactly include every expense or expand on the details of how they came to that estimate.

That’s because mortgage companies, to include the ones that offer calculators, are in the business of selling homes. So while monthly payments can be pretty large sums of money, mortgage companies don’t want you to think that (at least not initially). The last thing they want is for a potential buyer to be overwhelmed with sticker shock before even talking to a realtor.

So, to put homebuyers at ease, they provide mortgage calculators — easy, plug-and-play tools that make homeownership appear affordable.

Unfortunately, however, this is far from the truth. As explained below, mortgage calculators are never 100% accurate and homeownership isn’t as affordable as they make it seem.

How Mortgage Calculators can be Misleading

It’s important to remember that mortgage calculators as tools aren’t completely incorrect and they’re not trying to purposefully miscalculate your mortgage, but their estimates can be somewhat misleading.

Usually, mortgage calculators strategically leave out important costs and information, providing users with a best-case scenario. This gives online shoppers a false sense of affordability, leading homebuyers, and especially first-time homebuyers, to think they can afford a pricey home when they probably can’t.

The reason they do this, it seems, is to channel users to a particular mortgage site — kind of like some form of advanced clickbait.

And again, they aren’t lying and their calculations aren’t necessarily incorrect, but they leave out some pretty important costs that could significantly increase monthly payments.

To understand this in more detail, here’s a full breakdown of how some mortgage calculators (but not all) can be misleading for people trying to purchase a home.

1. Most Mortgage Calculators Assume You’re Putting 20% Down

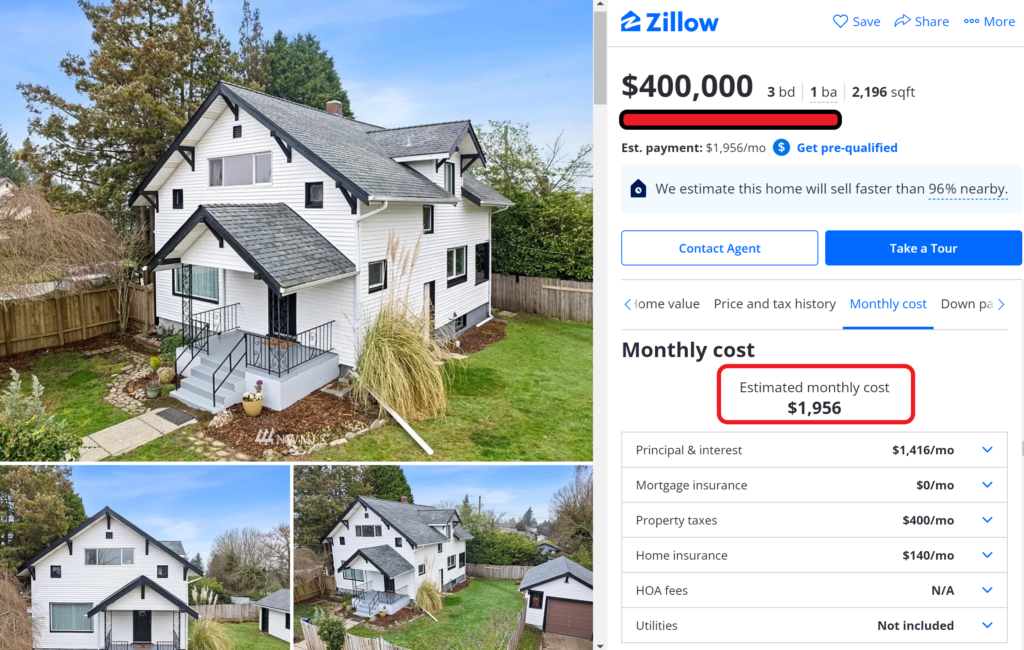

Most mortgage calculators automatically assume and populate a 20% down payment when you click on a house or enter in a particular price. Such is the case of the Zillow house below, where the current price of the home — $400,000 — is shown at the top of the page and an estimated monthly payment (with 20% down) — of $1,956 — is shown below it.

This isn’t necessarily wrong or incorrect (after all, it is just an estimate) but it’s not exactly accurate for everyday homebuyers — as 52% of non-cash homebuyers and 74% of new homebuyers make a down payment of less than 20%.

So, if we were to adjust the down payment to something that more accurately reflects the down payment of a first-time homebuyer, say 7%, then the monthly payment goes to $2,423 – precisely $467 more a month.

And of course, there is the option to expand the details of your “estimated monthly costs” and input the correct information yourself, but as a first-time homebuyer, this probably isn’t going to enter your head before reaching out to the realtor.

Thus, this is one of the main issues with mortgage calculators. At first glance, they give homebuyers a best-case scenario price, causing many homebuyers to search for houses that are outside their price range.

So why do calculators automatically populate 20%? Well, the only people who truly know the answer to this are the developers of the application and/or the team of marketers who worked on it. But there are two general theories:

- Theory 1: When a homebuyer thinks it’s affordable, they’re more likely to pursue it — so by showing potential homebuyers a best-case scenario when it comes to monthly payments, companies like Zillow are able to generate leads to real estate businesses or direct users to loan companies.

- Theory 2: Traditionally, 20% down is the historical standard and what banks prefer. However, as stated above, in today’s environment, most homebuyers put down less.

2. Mortgage Calculators Don’t Factor in Every Expense

It’s impossible to calculate your exact monthly payments using a mortgage calculator. In fact, you won’t know the exact amount until closing time. But, if you are going to use one, it’s best to use one with multiple input fields.

If you see a calculator that only has three or four options — such as home price, down payment, loan program (30 year or 15), and interest rate — it’s probably best to avoid it. It’s not including those “overlooked fees” that can greatly increase your monthly payments.

At the very least, a good mortgage calculator should have all the fields listed above — home price, down payment, loan program, and interest rate — but should also have input fields for credit score, property taxes, homeowners insurance, PMI (if applicable) and Homeowners Association (HOA) fees.

All of these expenses are important to factor into your calculation because more often than not, one or more of these factors will cause your monthly payment to go up.

3. Mortgage Calculators Don’t Factor in Closing Costs

Closing costs are pretty brutal and can catch any first-time homebuyer off guard.

These are one-time costs that come right before buying a home and include things like appraisals, title insurance, surveys, etc. Inspections are generally not considered closing costs but are another big-time upfront cost.

For obvious reasons, mortgage calculators don’t include closing costs because after you purchase your home, they won’t be part of your monthly payment. But, even though they’re one-time payments, they also shouldn’t be overlooked.

While there is some room for negotiation between you and the seller on exactly who has to pay what, closing costs can be a lot and they typically come out of the buyer’s pocket.

That means that whatever savings you’ve put together for a down payment, you’ll also need to factor in closing costs even though they’re not going to be reoccurring.

So whenever you go to put your down payment estimate into a calculator, remember to think about closing costs too. The last thing you want to do is overestimate how much you have available for a down payment.

4. Mortgage Calculators Can’t Predict Your Interest Rate

Similar to how mortgage calculators assume you’re going to put 20% down, they also assume your interest rate will be low and they automatically populate the best rate available. This is misleading.

Depending on your credit score, employment history, home location, down payment, loan amount, loan term, interest rate type (fixed or adjustable), and loan type (FHA, Veterans, Traditional, etc.), this can greatly vary from person to person.

To use an example, let’s say that we increased the interest rate of the Zillow house profiled above from 3.5% (what they have automatically populated) to 4.5%, only one percentage point higher. This “small adjustment” increases your monthly payment from $1,956 to $2,162, making your monthly payment $206 more a month.

So while a small change in a mortgage interest rate might not seem like a big deal, in some cases, it can increase your payment by hundreds of dollars. Be careful.

5. Mortgage Calculators Don’t Include Utilities or General Maintenance

Utilities and general maintenance on your house are two pretty significant costs that can greatly impact what you pay a month. They’re also not included in mortgage calculators.

A mortgage calculator won’t calculate these payments because they “technically” have nothing to do with your mortgage. But make no mistake, they will be just as big of a burden.

Depending on your house — age, structure, insulation, size, appliance efficiency — your utilities could run pretty high and they’re not exactly uniform payments; they change by the month. Additionally, if you’ve bought a fixer-upper, expect general upkeep and maintenance to be more than originally anticipated.

Unfortunately, for the buyer, it’s just how the game goes. Utilities and maintenance costs can stack up quickly so make sure to include them in your calculations.

6. Mortgage Calculators Typically Leave Out Flood Insurance

Flood insurance isn’t nearly as expensive as regular homeowner’s insurance, but if your house falls within a floodplain (or if you want flood insurance just to be on the safe side) then you’re going to have to pay a little extra a month.

Mortgage calculators, for whatever reason, don’t include flood insurance costs. And although there is occasionally an option to put in extra insurance costs, generally, it’s not going to be there.

If you’re wanting or needing flood insurance, it’s something that you’re going to want to factor in when calculating your monthly payments. If the home you’re looking at is teetering on the edge of affordability, flood insurance may be the one thing that knocks it out of your price range.

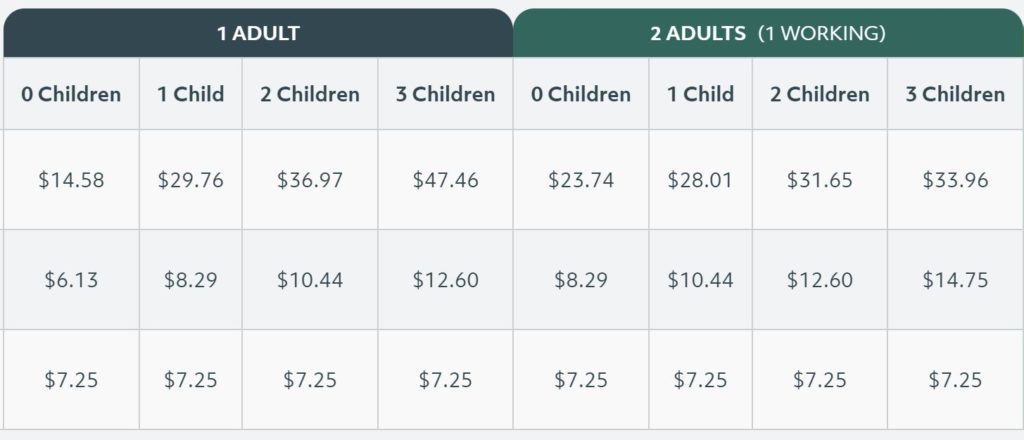

7. Mortgage Calculators Don’t Care About a “Living Wage”

As a general rule of thumb, you shouldn’t be paying more than 30% of your income on housing. That means that if you have an after-tax monthly income of $5,000, you’d want your monthly mortgage payment (with utilities included if possible) to be less than $1,500 every month.

That, however, as we all know, is getting harder and harder to do in today’s environment. That’s why it’s important to factor in your “living wage” before putting anything into a mortgage calculator.

And what is a living wage?

A living wage, by definition, is the real or actual wage needed to meet the minimum standards of living in your community. So while the minimum wage is the same for everyone in a given location, a living wage varies by person.

A living wage looks at individual circumstances and includes things like number of dependents, number of working adults in one house, childcare, transportation costs, medical costs, and food. That’s why the living wage, by all accounts, is a better indicator of affordability.

So before putting anything into a mortgage calculator, remember that your monthly income is just a number. Your “living wage” is what really determines if you can actually afford a house.

Most Accurate Mortgage Calculators and Tools

The best thing you can do to calculate your monthly payments is to use a good, old-fashioned excel spreadsheet.

An excel spreadsheet allows you to put in all of your information — to include those pesky payments that fall outside your mortgage payments — into an easy-to-read, comprehensive format. It’s effective, circumstantially-based, and unique to your financial situation. You can download one here or you can search for one on Google.

But, if you’re going to use a mortgage calculator anyway, try to use one that has a variety of fields and options so that your estimate is as close to accurate as possible. Additionally, if you’re a first-time homebuyer, just remember that expenses go beyond what they estimate. Make sure to use some other tools — such as the living wage calculator — to accompany your calculations.

Here’s a quick list of mortgage calculators and tools worth using:

Mortgage Calculator

Mortgagecalculator.org has one of the more comprehensive and complete mortgage calculators. It includes a total of 12 input fields so that users can calculate those often “overlooked” expenses when buying a house.

Bankrate Mortgage Calculator

The mortgage calculator from Bankrate has an easy-to-use dashboard that includes a payment breakdown pie chart. Enter your initial loan information and then click “advanced options” to put in the rest of your information. Once calculated, be sure to hit the “amortization schedule” to see how to pay off your home faster.

Living Wage Calculator

Use the living wage calculator to see what it “realistically” takes to financially succeed in your community. The living wage calculator factors in circumstantial information — number of working adults per household, cost of food, number of dependents, etc. — and then calculates the minimum hourly wage you need to financially get by. Use this with other calculators to see what you can afford.

Millennial Cities

Want free articles, news, tools, and information? Subscribe below and we’ll add you to the list!